Quick answer: A covered call is an options strategy where an investor owns a stock and sells a call option against that position. The investor collects premium but agrees to sell the stock at the strike price if assigned. Covered calls are a conditional tool: they cap upside and leave you holding most of the downside, but on the right stock, with a rich enough premium and disciplined management, an overlay can enhance returns.

Last updated: May 29, 2026 — Belanger Trading reviews this page as options-market conditions and our framework evolve.

The “easy income” pitch, and what it leaves out

Covered calls sound like easy income. Own the stock. Sell the call. Collect the premium. The premium is real — and so is the tradeoff most investors ignore. That does not make the strategy bad; it makes the lazy story around it bad.

So carry one idea through this page: a covered call is long stock plus short volatility. You keep most of the downside, give away the upside, and the premium only helps if the option was priced rich relative to the risk you took on. Understand that tradeoff and a covered call becomes a tool you can use intentionally — on the right stock, with the right strike and a real management rule, it can enhance returns. Used blindly on every stock, it quietly punishes your best ideas. Every great trade or investment starts with deep research.

The appeal is genuine — premium up front, a supplement to dividends, cash flow on stock you already hold, a way to set an exit price you’d be happy with, a small cushion on minor drops. None of it is false, just incomplete. The premium is not free: you are paid for giving away your upside above the strike — a known modest amount today for an unknown, potentially large gain you may never see. The strategy is not the problem; running it on a stock you own for the upside is.

What is a covered call?

A covered call has two pieces. First, you own the stock — usually at least 100 shares, because one option contract covers 100 shares. Second, you sell (write) a call against those shares, giving the buyer the right to purchase your stock at a set price (the strike) before a set date (the expiration). For that you collect a premium up front. The catch is the obligation: if the stock rises above the strike, the buyer can exercise and your shares get called away at the strike, no matter how high it climbed.

A plain example. You own 100 shares of a $50 stock and sell one $55 call for $1.50, collecting $150. Stay below $55 at expiration and the call expires worthless — you keep your shares and the $150. Rise above $55 and your shares are sold at $55: you keep the $150 plus the $5-per-share gain up to the strike, but nothing above. If the stock is at $70, that is $15 a share — far more than the $150 premium — that you never see. That is the real exchange covered-call write-ups rarely put a number on.

Not free income, and not downside protection

Two pitches make covered calls sound better than they are: that the premium is income, and that it protects you on the downside. Both fall apart under scrutiny.

Premium received does not automatically equal profit. AQR Capital Management’s paper “Eight Myths and One Fact About Covered Calls” (Roni Israelov and Lars Nielsen, June 2014) argues a covered call is best understood not as income, but as equity exposure plus short-volatility exposure (AQR / SSRN). You run two bets at once: the bet that stocks rise over time (the equity risk premium), and a bet selling insurance on volatility (the volatility risk premium), which only pays off if options were priced richer than the movement that actually shows up. AQR’s stylized example (hypothetical, by design): an index at $100, a one-month at-the-money call, implied volatility of 18% against realized volatility of 16%. The call sells for about $2.07, but only about $0.23 — roughly 11% — is the genuine “extra” from selling volatility rich; the rest is just the arithmetic of holding less stock. Had implied volatility equaled realized, you would collect a fat premium but earn zero volatility risk premium. It is compensation for risk, not a gift.

Nor is a covered call “safer” or “lower risk” than owning the stock. It can reduce some exposure, but it does not remove the stock risk — you keep most of the downside and give away the upside. AQR studied the Cboe S&P 500 BuyWrite Index (BXM), which systematically writes one-month at-the-money calls on the S&P 500, over July 1986 through December 2013. BXM earned roughly similar returns at about two-thirds the volatility, which sounds protective — yet it still drew down about −43% in that window (less bad than the S&P’s roughly −62%, but brutal, not protected). The asymmetry is the load-bearing fact: BXM’s downside beta was about 0.78 while its upside beta was only about 0.63 (AQR / SSRN). It captured less of the up moves than it absorbed of the down moves. These are historical illustrations over a stated window — not a forecast, and not a Belanger Trading track record.

Why covered calls and cash-secured puts are similar

A covered call and a cash-secured put (or naked short put) are economically close cousins: both collect premium, both cap upside, and both leave you holding most of the downside. AQR makes the point bluntly — a short put is essentially equivalent to a covered call, so the “sell a put to buy the dip at a discount” pitch is the same sleight of hand as “covered call for free income” (AQR / SSRN). Different starting point, same underlying bet: long the stock, short volatility. For the put side, see our companion page on cash-secured puts.

The problem with “lowering your cost basis”

A popular pitch says you can sell calls month after month, bank the premium each time, and steadily grind your cost basis down to nothing. It sounds like a flywheel. It is not. That story quietly assumes the stock never gets called away, never rallies too far above your strike, and never falls hard enough that the premium stops mattering. If the stock rallies through your strike, you are forced to choose: let the shares go, or buy the call back at a loss to keep them. If it falls sharply, the premium barely dents the drawdown. Selling a call collects cash, but it does not change the underlying fact — you own the stock, you keep the downside, and you sold away part of the upside. “Lowering your cost basis” is bookkeeping, not protection.

Two reasons to own a stock — and which one calls fit

Josh Belanger frames the decision with a simple question: why do you own this stock in the first place? Investors buy a stock for one of two reasons — for the dividend income it throws off, or for the appreciation they expect from the price.

That answer should decide whether you write calls against it. If you own a stock for appreciation, selling calls can handicap the exact reason you bought it: the trade caps your upside, and a big move — the move you were positioned for — gets called away. If you own a stock for income and you are genuinely willing to sell it at a target price, a covered call can make more sense; you are getting paid to set an exit you would have taken anyway. Same structure, different stock, different result. The covered call is not good or bad in the abstract. It depends on the stock, the thesis, the premium, and the objective.

When covered calls can actually work: the Realty Income example

A real name makes it concrete. Realty Income (NYSE: O) calls itself “The Monthly Dividend Company” — a net-lease REIT that pays monthly and has raised its dividend for more than 100 consecutive quarters, with a yield near 5% as of early-to-mid 2026 (Realty Income SEC filings). It is a stable, low-volatility income stock, so its options carry low implied volatility — thin premium, little “extra” to collect. By the AQR lesson, if implied vol sits close to realized vol, that premium is not really economic income.

So is O a poor covered-call candidate? Low-volatility dividend stocks can be poor candidates — but only when the premium is too small relative to the upside being given away and the capital tied up. That is a conditional verdict, not a blanket one. Whether the trade works depends on how the premium stacks up against the opportunity cost over time. So we ran the numbers.

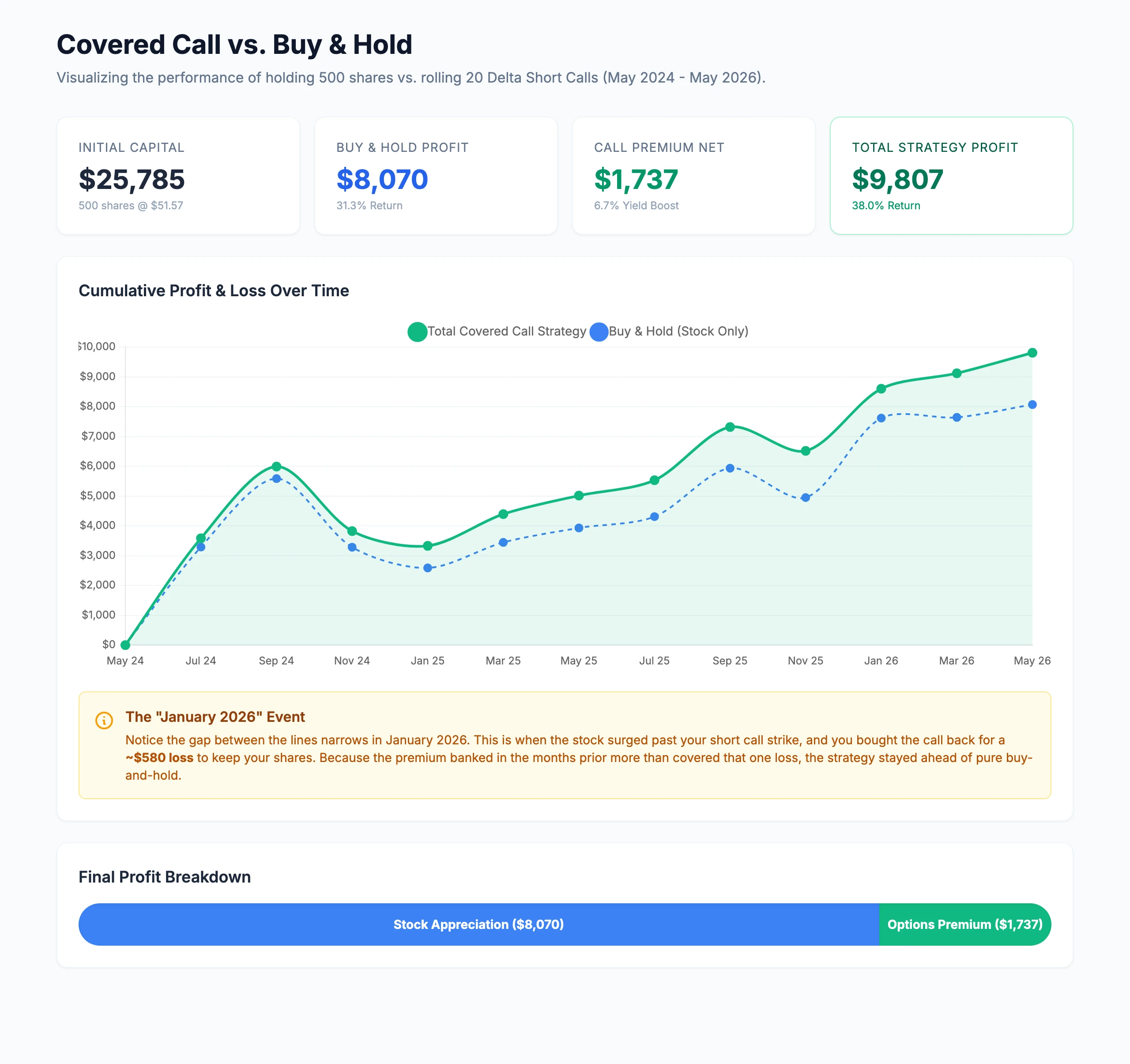

We ran one historical Belanger Trading backtest on O to pressure-test the conditional case. The setup: start with $25,785 — 500 shares of Realty Income bought at $51.57 in May 2024 — and hold those shares through May 2026 while running a covered-call overlay on top. The overlay sold rolling 20-delta short calls roughly 60 days to expiration, bought them back at 50% of maximum profit, and redeployed into the next call. This is a modeled strategy on historical prices; it excludes commissions, taxes, and slippage.

Here is how the two-year period broke down:

- Buy-and-hold: owning the 500 shares outright returned $8,070 — a 31.3% gain, including capital appreciation plus the monthly dividends.

- Net call premium: the covered-call overlay added $1,737.50 in net premium after buybacks — about 6.7% on the initial capital.

- Total strategy: $9,807.50, a 38.0% return — the buy-and-hold result plus the overlay.

Two trade cycles show the mechanics — one ordinary win and the one that hurt.

- A standard win. On July 19, 2024 the model sold 5 calls at the $62.50 strike for $0.25. By September 20 the stock sat at $61.63 — just under the strike — and the calls were bought back at $0.02, locking in roughly $115 of premium while keeping the shares and their upside.

- The notable loss. On November 21, 2025 the model sold 5 calls at the $60 strike for $0.30. By January 16, 2026 the stock had rallied to $61.42, pushing the calls in-the-money; to avoid assignment they were bought back at $1.45 — a realized options loss of roughly $575 on that cycle.

The January 2026 cycle is the point: when a stock breaks above your strike, there is no free lunch — you choose between letting the shares be called away, buying the call back at a loss, rolling it out, or accepting the capped upside. The overlay only came out ahead because, across the full two years, the premium collected on the many quiet cycles outpaced the drag from that one major loss, and because the shares were bought back rather than called away, the position kept its stock appreciation.

Belanger Take

This is the right way to think about covered calls: not free income, not downside protection, and not a strategy to run blindly on every stock — a conditional overlay that can enhance returns when the stock, the premium, the strike selection, and the management rule all line up. It worked on O over this window because the premium outpaced the one major loss and the shares were never permanently called away. It would not necessarily work on a stock owned for explosive upside: run this same overlay on an NVDA, PLTR, or TSLA position you hold for the appreciation, and a single rally through the strike can cost you far more than every premium you ever collected.

Covered-call ETFs: income candy with tradeoffs

If you would rather not run the overlay yourself, funds like JEPI, QYLD, and XYLD package the strategy and advertise eye-catching distribution yields — roughly 8% for JEPI and double digits for QYLD and XYLD as of mid-2026, all approximate (TrendSpider comparison). The headline numbers are the draw, and they deserve a skeptical read. The same AQR lesson applies at the fund level: a high distribution yield is not a high total return. These funds systematically sell away upside, charge a fee, and run a rules-based options strategy — so the yield is partly the volatility risk premium and partly just the return of capital from giving up appreciation, and total return can structurally lag the index in a strong bull market.

But they are not all the same, and the differences matter: the fee, the underlying index, how far out-of-the-money the calls are written, the call-writing methodology, execution quality, and the market environment all change the outcome. A fund writing out-of-the-money calls on a slice of the portfolio keeps more upside than one writing at-the-money calls on all of it, and some of these strategies do better in flat or range-bound markets than in a roaring bull run. They can have a place — but the place is decided by the methodology underneath, not the headline yield. Belanger Trading is cautious here: do not buy a covered-call ETF on its advertised distribution rate alone.

Covered calls vs cash-secured puts vs short put spreads

A covered call is one of several ways to collect premium with a bullish-to-neutral view:

| Strategy | Upside | Downside | Capital use | Best for |

|---|---|---|---|---|

| Own the stock | Full rally, uncapped | Large, bounded — down to near-zero | High — full share price | Long-term ownership and full upside |

| Covered call | Capped at the strike (plus premium) | Large, bounded — stock to near-zero, minus premium | High — you hold the shares | Income on stock you’d sell at the strike anyway |

| Cash-secured put | Capped at the premium | Large, bounded — (strike − premium) × 100 | High — strike × 100 set aside | Wanting to own lower; idle cash |

| Short put spread | Capped at the net credit | Capped at width − net credit (defined) | Low — defined risk | Defined-risk premium income |

Read the downside column carefully. For a covered call, the loss is bounded, not unlimited — you own the stock, so the worst case is it falling to near-zero, minus the premium. (The “unlimited loss” warning belongs to a naked call, where you sold a call without owning the shares — a genuinely riskier animal.) What a covered call actually caps is the upside. For premium income we generally prefer the last row — a defined-risk short put spread, which does not remove risk but defines it, capping the loss up front and freeing capital instead of tying up a full share position. That is the lane Belanger Trading’s 48 Hour Income approach lives in.

When it works — and when it backfires

Written with eyes open, a covered call does a real job when most of these hold: you are a genuinely willing seller at the strike, the stock is fully valued so the far upside costs little to give up, you expect a range (flat-to-mildly-up is where covered calls earn their keep), and your goal is income, not maximum growth. Tax or retirement-income considerations can tip the scale too — steadier cash flow from a position you’d hold anyway has value. (Talk to a tax professional; that is not our lane.)

The mirror image is where the trade turns on you: the stock rallies sharply through your strike and a big gain gets called away; you feel assignment regret and are out of a winner; the premium was too small to justify the upside surrendered and the capital tied up; or a catalyst surprises to the upside — a buyout, a blowout quarter — and you capped exactly the move you owned the stock for. The common thread: used blindly, covered calls quietly punish your best ideas. The position you were most right about is the one most likely to blow through the strike.

The Belanger Framework for covered calls

- Know why you own the stock — for income or for appreciation. If it is appreciation, think hard before capping it.

- Decide if you are truly willing to sell at the strike. If not, do not write the call.

- Compare the premium against the upside you surrender and the capital you tie up — not just whether it “looks good.” A fat premium prices in real risk; it is not a free gift.

- Understand you are selling volatility — the trade pays extra only if implied vol was rich versus what shows up.

- Know your exit before you enter — roll, take assignment, or buy back. Decide in advance, as the backtest’s discipline (buy back at 50% profit) shows.

- Ask whether a defined-risk spread expresses the view better — often it uses less capital for a known risk. And remember: cash flow is not profit.

FAQ

Are covered calls safe? No options strategy is “safe,” and a covered call is not “safer” than owning the stock. It can reduce some exposure — the premium offsets a sliver of any decline — but it does not remove the stock risk. You keep most of the downside and give away the upside. It softens the blow; it does not eliminate the risk.

Can you lose money with a covered call? Yes. You own the stock, so a hard fall is your loss minus the small premium. The loss is bounded — the stock can only fall to zero — but it can be large. What is capped is your upside, not your downside.

Do covered calls generate income? They generate cash flow, which is not the same as income or profit. The premium is genuine “extra” only to the degree the option was priced rich versus the volatility that actually shows up (AQR / SSRN) — otherwise it is just the math of owning less stock.

Covered call vs cash-secured put — which is better? They are economically similar: both collect premium, cap upside, and keep most of the downside. The choice is mostly your starting point (shares you own versus cash set aside) and your tax and account situation. See cash-secured puts for the put side.

What happens if the stock rises above the strike? Your shares can be called away at the strike. You keep the premium and the gain up to the strike but forfeit everything above it. In a sharp rally, the surrendered upside can dwarf the premium — which is exactly why the stock you own for the upside is the wrong one to write calls against.

Where to go next

New to options income? Start with the free Options Trading Starter Kit. For the defined-risk approach in practice, 48 Hour Income focuses on premium-selling with risk defined up front. To see what large options traders are doing with real money, read unusual options activity. And because covered calls only work on stock you actually want to own, start with the right portfolio underneath — our best stocks to buy now research.

What this page is not

Belanger Trading publishes research and analysis for informational purposes. Nothing on this page is personalized investment advice. Options carry risk, are not appropriate for every investor, and can result in loss of principal. The examples are illustrative, ignore commissions and fees, and are not quotes or recommendations. The AQR figures and Cboe BuyWrite Index (BXM) statistics are historical illustrations over a stated window (primarily July 1986 through December 2013) — not forecasts and not a Belanger Trading track record. The Realty Income and covered-call-ETF figures are point-in-time readings that move daily; refresh them before acting.

The Realty Income covered-call figures (May 2024–May 2026) come from a single historical Belanger Trading backtest. It models a specific approach — holding 500 shares while selling rolling 20-delta short calls roughly 60 days to expiration, bought back at 50% of maximum profit and redeployed — applied to historical prices. It excludes commissions, taxes, and slippage, which would all reduce the result. The backtest is illustrative and educational only. It is NOT a track record of client results, NOT a recommendation, and does NOT imply the same approach would work on any other stock, ETF, or in any other market environment. Past performance does not guarantee future results. Consult a licensed financial advisor before making any investment decision. As of publication, neither Belanger Trading nor its research desk discloses a position in the securities discussed unless stated otherwise.

Sources

- Covered call as equity exposure plus short-volatility exposure; the “one fact”; the at-the-money covered call ≈ ½ long stock + ½ short straddle decomposition; the stylized example (implied 18% vs realized 16%, ~11% of premium as the volatility risk premium); the “income is not automatic profit” and “no real downside protection” points; covered-call ≈ short-put equivalence — Roni Israelov and Lars N. Nielsen, “Eight Myths and One Fact About Covered Calls,” AQR Capital Management, June 2014: SSRN abstract 2444993

- Cboe S&P 500 BuyWrite Index (BXM) vs S&P 500, July 1986–December 2013 (similar return at ~two-thirds the volatility; worst drawdown ~−43% for BXM vs ~−62% for the S&P; upside beta ~0.63 vs downside beta ~0.78) — same AQR paper, Table 1: SSRN abstract 2444993; index methodology background: Cboe BXM Index dashboard

- Realty Income (O) monthly-dividend profile, ~$3.25 annualized dividend and ~5% yield (early-to-mid 2026; moves with price) — Realty Income SEC filings (EDGAR)

- Realty Income covered-call overlay results (500 shares from $51.57, May 2024–May 2026: buy-and-hold $8,070 / 31.3%; net call premium $1,737.50 / 6.7%; total $9,807.50 / 38.0%) and the July 2024 and November 2025 trade-cycle examples — Belanger Trading historical backtest on price and option data; modeled rolling 20-delta ~60-DTE short calls bought back at 50% profit; excludes commissions, taxes, and slippage; illustrative, not a track record

- Covered-call ETF distribution yields and the yield-versus-total-return tradeoff (JEPI ~8%, QYLD and XYLD double-digit, all approximate, mid-2026) — TrendSpider: JEPI vs QYLD vs XYLD covered-call ETF comparison